Editor’s Note: This is Part 2 of an ongoing series examining the structural forces behind Nigeria’s declining student emigration. Part 1, published in the Diaspora Lens on LinkedIn, established that the “Japa slowdown” is not evidence of improved local universities. It is a direct consequence of the tightening of immigration policy in the UK, Canada, and the US. This piece follows the money.

There is a young man somewhere in Lagos right now, let’s call him Emeka, who finished his economics degree two years ago with a second-class upper. He has applied to three master’s programmes in the United Kingdom. His father sold land in Delta State to help fund the process. His visa was denied twice: once over a documentation discrepancy, once over financial verification. He is not an anomaly. He is the policy.

UK Home Office records show that in the first six months of 2024 alone, Nigerian students received just 4,669 main applicant study visas, compared with 14,772 in the same period the year before. That is a 68% collapse in six months. In Canada, the Nigerian student approval rate shrank from 38% in 2022 to just 18% in 2024, even before Ottawa announced a two-year cap on international study permits that drove overall issuance down by 35%.

When official voices in Nigeria look at those numbers and declare them evidence of a domestic education renaissance, Emeka knows the truth. So does his father, who is still waiting to be repaid for that land.

But here is where the story gets harder and more complicated. Because even if the visa doors were flung wide open tomorrow, Emeka would come home to a job market that cannot absorb him. The same policy reforms that made his plane ticket unaffordable have systematically dismantled the domestic economy that was supposed to catch him if he stayed.

This is not two separate problems. This is one pincer.

I. The Night the Numbers Tripled

To understand what happened to Nigeria’s corporate sector, you have to understand what June 2023 meant on a balance sheet.

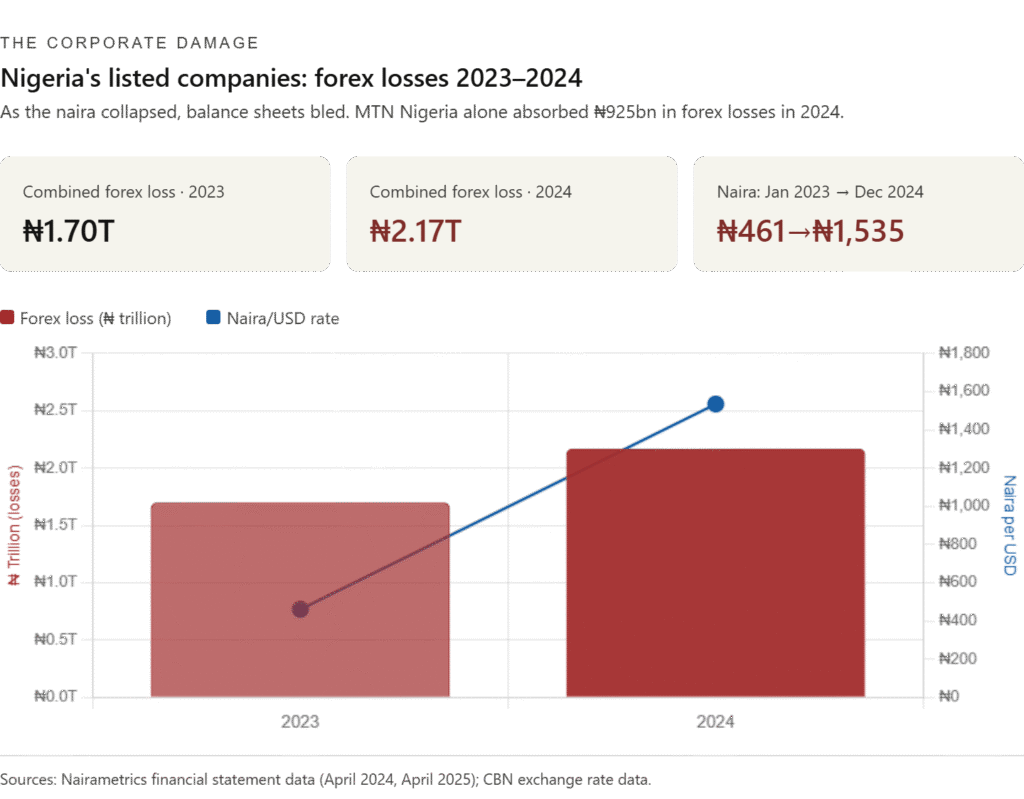

When President Tinubu’s administration launched its foreign exchange unification policy and floated the naira, it did not just change a number on a screen. It detonated the debt obligations of every Nigerian company that had borrowed in US dollars when the exchange rate was still manageable. The naira opened 2023 at ₦461.50 to the dollar. It closed the year at ₦907.11. By the end of 2024, it stood at ₦1,535.

In less than eighteen months, the cost of servicing a dollar-denominated loan in naira terms more than tripled.

The casualties were not small. According to financial statement data collated by Nairametrics, Nigeria’s leading listed companies incurred a combined forex loss of ₦1.7 trillion in 2023 alone. These were losses so severe they effectively wiped out the shareholder funds of some firms and forced mega-restructuring for others. By 2024, that collective figure had climbed further to ₦2.17 trillion.

MTN Nigeria is the most instructive single case study. Nigeria’s largest telecommunications company, the infrastructure backbone of the country’s digital economy, reported a loss after tax of ₦400.44 billion for 2024, a staggering 192% increase from its ₦137.02 billion loss in 2023. Its forex losses alone reached ₦925 billion that year. MTN’s revenue actually grew by 36% over the same period. The company was performing well by most operating measures. The currency simply turned that performance into a reported loss on paper and a very real crisis in planning, investment, and hiring.

For consumer goods firms, the damage was proportional. Nestlé Nigeria recorded ₦195 billion in forex losses. Nigerian Breweries absorbed ₦153.3 billion. An analysis of eight major consumer goods companies showed their combined forex loss in 2023 alone amounted to ₦839.24 billion, more than 18 cents of every naira they earned in revenue, evaporated by exchange rate arithmetic before a single bottle left the factory.

When a company is haemorrhaging that kind of money simply because a currency moved, it does not build new factories. It does not open new divisions. It does not post entry-level roles. It survives.

The immediate casualty of corporate survival mode is always the same: the graduate waiting at the gate.

II. The Money Is There. Look Where It Goes.

Here is where the story becomes genuinely infuriating.

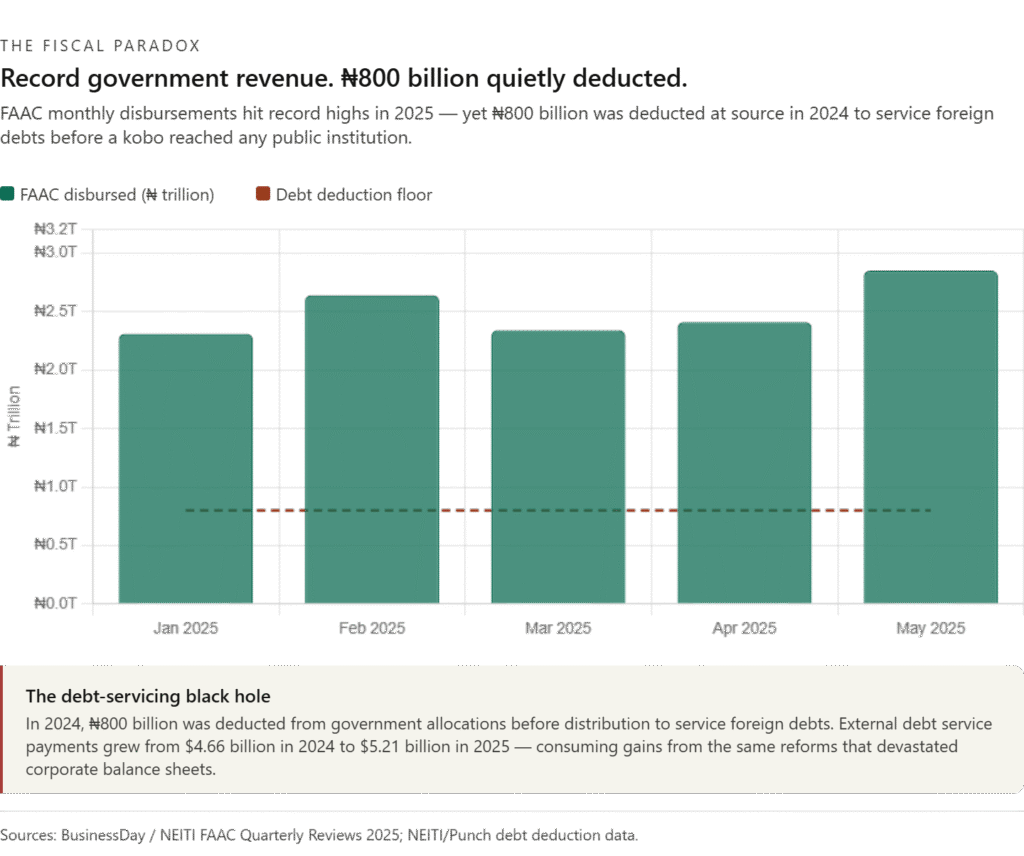

By any measure of raw revenue, the Nigerian government is currently making more money than at any point in the country’s history. The same reforms that decimated corporate balance sheets – fuel subsidy removal and currency float – dramatically boosted government oil revenue remittances and naira-denominated FAAC receipts.

The Federation Account Allocation Committee disbursed ₦2.31 trillion to the three tiers of government in January 2025. By May, that monthly figure had reached ₦2.85 trillion. Across the first eleven months of 2025, total FAAC disbursements hit ₦33.27 trillion, a 30% increase on the same period in 2024, itself already a record year. Q3 2025 alone saw ₦6 trillion disbursed in a single quarter, described by the Nigeria Extractive Industries Transparency Initiative (NEITI) as the highest quarterly disbursement ever recorded.

The Federal Government received ₦2.19 trillion of that Q3 figure. States received ₦1.97 trillion. Local governments, ₦1.45 trillion.

Record money in. So why are public university laboratories still running on 1990s equipment? Why do nursing students still graduate without handling functional diagnostic tools? Why are research centres competing with local markets for internet bandwidth? Because of what happens before those numbers reach any ministry.

In 2024, ₦800 billion was deducted from government allocations at source, before distribution, to service foreign debts and other contractual obligations, according to NEITI data. The deductions have continued rising. External debt service payments grew from $4.66 billion in 2024 to $5.21 billion in 2025. And the compound problem is this: the naira in which those numbers are reported is worth far less than it was when the original debts were contracted. The government is collecting record naira revenues while repaying legacy dollar debts at a structurally disadvantaged exchange rate.

The revenue gains from harsh reforms are being vacuumed directly into servicing the borrowing decisions of previous and current administrations. There is no fiscal oxygen left for university infrastructure, curriculum reform, or the kind of sustained research investment that makes a domestic graduate economy viable.

You cannot point to record FAAC disbursements and claim the educational sector is thriving. That is not revenue reaching classrooms. That is revenue reaching creditors.

III. The 93% Problem Nobody Is Talking About

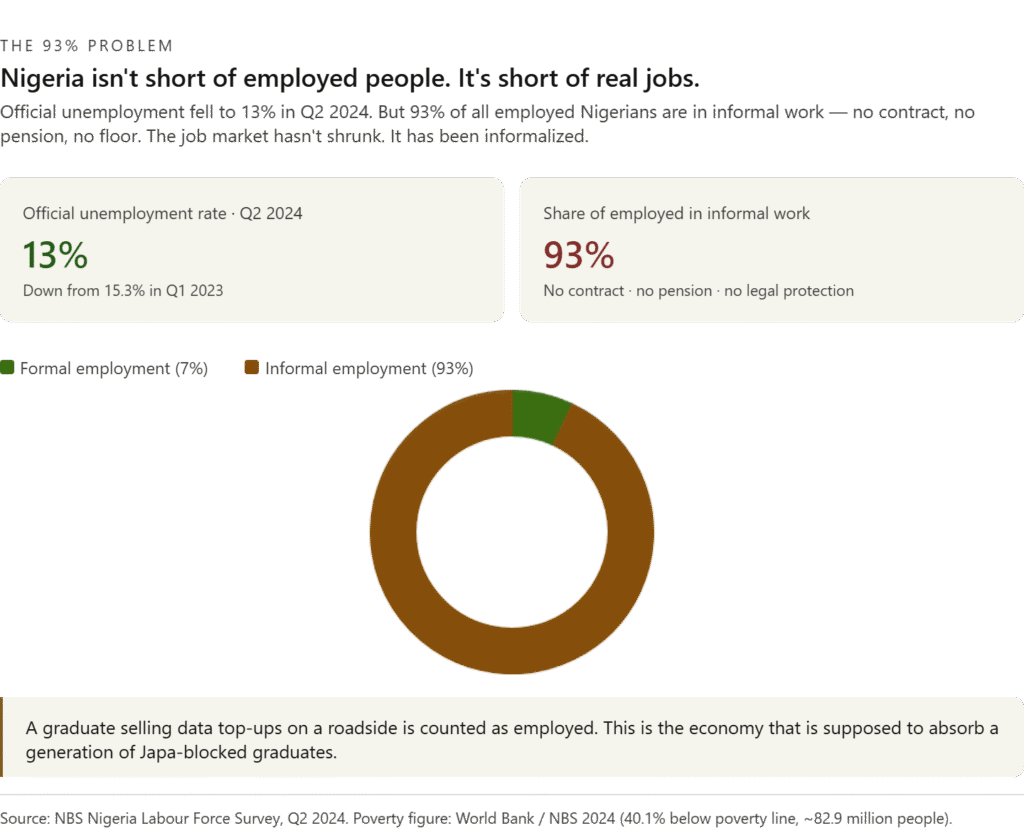

Here is a statistic that reframes the entire debate about Nigeria’s job market, and it comes directly from the National Bureau of Statistics.

Official unemployment figures in Nigeria show a declining rate. The combined unemployment and underemployment rate dropped to 13% in Q2 2024 from 15.3% in Q1 2023. At first glance, that reads as progress.

But look at what sits inside that employment figure. Informal employment in Nigeria stands at 93%. That means nine out of every ten Nigerians counted as “employed” are working without contracts, without protections, without pension contributions, and without the stability that allows a person to build a life. A fresh economics graduate selling mobile data top-ups from a roadside kiosk is counted as employed. A nurse working for a private clinic that pays ₦40,000 a month with no benefits is counted as employed.

The Nigerian job market has not been shrinking so much as it has been informalized, and informalization at this scale is a more accurate description of structural failure than unemployment numbers alone can capture.

This is the economy that is supposed to absorb Emeka.

Meanwhile, 40.1% of Nigerians, approximately 82.9 million people, live below the poverty line. That figure is not a backdrop statistic. It is the aggregate outcome of the very corporate squeeze and fiscal misalignment that this piece documents. The poverty line does not record intent. It records consequences.

IV. The Curriculum That Trains Graduates for Jobs That Left

The Ministry of Education is right about one thing: local universities are seeing more applicants. What it won’t say out loud is why.

When the UK slams a door on 70% of your applicants in six months, when Canada’s Nigerian approval rate drops to 18%, when the US adds “heightened scrutiny” to the visa process for several African nationalities, of course, more students apply locally. That is not a demand. That is the default.

And what they find when they arrive locally is a curriculum architecture that has not been seriously reformed in a generation. Degree programmes that do not interface with the actual structure of Nigeria’s economy. Research departments without functional equipment. Universities whose operational budgets are consumed by maintenance of crumbling infrastructure rather than investment in learning.

The corporate sector that would have employed these graduates is running on survival budgets. The government that funds these universities is service-locked into debt repayments. The global doors that would have offered alternatives have narrowed to cracks.

A young person in this system is not failing to navigate the economy. The economy has been systematically drained of the capacity to receive them.

V. What a Structural Trap Actually Looks Like

Corporate executive Emmanuel King was right to shift the spotlight toward the macroeconomic ecosystem when he commented on Part 1 of this series. The diagnosis is worth stating plainly.

Nigeria’s youth are not caught between two bad options. They are caught in what analysts would call a structural trap, where the external escape valve (emigration) has been closed by host-country policy, and the internal absorption mechanism (formal employment) has been hollowed out by forex crystallization and debt-serviced governance.

Neither problem is temporary. UK immigration policy is not reversing course; visa applications from Nigerian students remain down, and the policy architecture that created the drop is still in place. Canada’s study permit cap is set to hold through 2026. And the ₦2.17 trillion in accumulated corporate forex losses do not resolve on their own. Companies that had their shareholder equity wiped out in 2023 and 2024 are rebuilding slowly, in a high-inflation, high-interest-rate environment, with no guarantee of currency stability going forward.

The question Nigeria’s policymakers need to be asked – publicly, specifically, and repeatedly – is this: if you cannot get young Nigerians out, and you have not built the conditions to absorb them in, what is the actual plan?

Record FAAC disbursements are not a plan. They are a number. Until ₦800 billion is no longer being siphoned from those disbursements before they reach any public institution, until corporate tax and debt restructuring policies are designed to incentivize domestic hiring rather than just stabilize balance sheets, until public universities receive capital investment proportional to the students they are now forced to accept, the structural trap does not loosen. It compounds.

The Verdict

Emeka is still in Lagos. His father’s land is still sold. His third visa application is still being processed.

There are hundreds of thousands like him, qualified, prepared, willing, and caught between an international system that does not want them and a domestic economy that cannot pay them.

The government that celebrates declining Japa numbers as a sign of national confidence should be asked to reconcile that celebration with this: a generation of graduates entering an economy where 93% of jobs are informal, where the companies that should hire them posted ₦2.17 trillion in losses in a single year, where record government revenues are being consumed by debts contracted before these graduates were in secondary school.

That is not a policy milestone.

That is a debt being passed forward, and young Nigerians are the ones holding the bill.

Sources

- UK Home Office Student Visa Data, H1 2024 (via Semafor, August 2024)

- Immigration, Refugees and Citizenship Canada (IRCC) permit data, 2024

- Nairametrics: “Leading Nigerian companies incur a staggering ₦1.7 trillion in FX losses in 2023” (April 2024)

- Nairametrics: “Ten Nigerian companies incur ₦2.17 trillion in forex losses” (April 2025)

- MTN Nigeria Plc Annual Report, FY2024 (February 2025)

- Veriva Africa: “Navigating the Storm: The Impact of Currency Devaluation on Nigeria’s Consumer Goods Industry” (April 2025)

- BusinessDay: “FAAC disbursement surges by 30% to ₦33.27trn in 11 months” (January 2026)

- NEITI Quarterly Review of FAAC Allocations and Disbursements, Q3 2025 (January 2026)

- NEITI / Punch: “FG deducts states’ ₦800bn allocations to pay foreign debt” (2025)

- National Bureau of Statistics (NBS): Nigeria Labour Force Survey, Q2 2024

- Punch: “Nigeria’s External Debt Consumes ₦136bn of January Revenue” (March 2026)

For incisive analysis decoding global power, politics, and culture through the African diaspora experience, visit Akatarian.com and subscribe to The Diaspora Lens newsletter.

{kind=link}